In the previous article we outlined the problem of position holding time and its relationships with the overall performance of trading strategies in cash currency markets. We have discovered that in case we hold positions for a longer time then generally the average trade value increases, which given the real market expenses such as spread, slippage and commissions, makes strategies more tradable. At the same time we have discovered that the volatility of returns in this case also increases proportionally which automatically increases the drawdowns and potentially may make a strategy not acceptable for production. Obviously the goal of a trading systems developer is to find a trade-off, a balance between reasonably large average trade values and acceptable volatility of returns. However this task can hardly be solved – at least if we mean consistency of returns over a multi-year time span – without taking into consideration various factors which may not have any direct relationships with the market process exploited by a strategy, but affect the behavior of markets in general, and in quite a long term perspective. We mean both behavioral patterns of market participants and market structure as such, and how it affects changes in market regimes which in turn impact the performance of trading strategies.

Identifying market regimes and especially changes in them is a very complex task which, to the best of our present knowledge, cannot be solved 100% formally, and thus it always requires a certain amount of discretion. The reason is that a market regime identification is mostly based on an analysis of qualitative factors, not quantitative, and besides that each of these qualitative factors should be assessed by its importance for the market in whole and for each particular market/trading strategy in it. The main problem here is that almost every time the market regime changes, such a change looks like something new, never observed in the past. There’s no surprise in it: typically factors which cause these changes – and in the first place these are changes in the regulatory environment which in turn cause changes in the market regime – are also unique and almost none of them is a repetition of the past, therefore a quantitative researcher would have had really hard time developing a model because there are virtually no samples of the same, or at least similar situation in the past to compare to.

Nevertheless we can use various “proxies”, or indirect semi-quantitative assessment to at least roughly estimate the importance of a given factor for a given market, and one of the best proxies of this kind is analysis of public resources such as professional discussion boards and forums which publish opinions on the current situation in the market. Speaking in very general terms, if we can see that a single subject has been heavily discussed by the professional audience for several months in regard to its potential impact onto market structure, then a trading strategies developer should definitely take it into account.

Although the problem of market regimes identification, especially for future changes in the market structure, lies outside the scope of this article, let’s consider just one example of probably the most significant change in the market regime which we observed in the last 15 years and how it changed the price behavior so radically that many known-to-be-good trading strategies stopped working completely. This change was caused by the implementation of Dodd-Frank act and its aftermath can be easily observed in the price behavior of many markets even today.

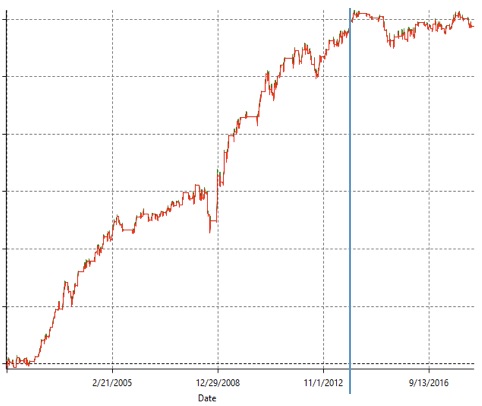

Let’s consider a simple momentum strategy which enters long only and holds a position for a number of days. This corresponds to typical investors behavior when new positions are opened in the direction of the price movement, especially if such a movement was originated by an important economical news. Let’s apply such a strategy to historical prices of the euro vs the US dollar and consider its performance in form of an equity curve.

The blue vertical line corresponds to the date when most of the rules in the act, including Volker rule with prohibition of proprietary trading, establishment of concentration limits and others came into force. We can see that a strategy which used to work reasonably well for many years before Dodd-Frank almost immediately stopped working at that time. Even the financial crisis of 2007-2009 didn’t have such an impact on its performance: indeed, the deep drawdown in 2008 is easily explained by the bearish market at that time, and the fact that this strategy is long only. Thus this drawdown was relatively quickly recovered and the strategy continued to perform well even at a higher rate, which again is not surprising given greater volatility which existed in markets those years. At the same time after Dodd-Frank the strategy stopped performing at all – not that is started to lose money, but its returns became almost random and therefore could not be accumulated for any reasonable gain.

We set aside here the discussion about how the implementation of Dodd-Frank actually affected this market because it could be too vast a topic for a single article, but in essence important changes in the market regime caused by new regulations typically impact the volatility profile, and it in turn has an immediate impact onto performance of directional strategies. Of course we should take into account many other factors, especially specific for a given market, such as interest rates policy, but very similar picture – dramatical change in volatility and price behavior after 2012-2013 – can be observed in many markets using similar simple research tools, so we can definitely speak of a major change caused by the new set of regulations.

Understanding these changes helps explaining why a particular strategy “suddenly” stopped performing in a particular market, but obviously we would like to also understand how to mitigate risks of this kind, how to keep the consistency of returns in the ever changing market environment. Actually the choice is not really wide: we have only two possibilities here – either to adapt to the new reality, or intentionally develop strategies which are less dependent on these global processes.

Adapting an existing trading strategy to a new market regime could be quite a complicated task because of the enormous number of factors to account for, and worst of all – because a change in the market regime is not something which happens in a moment; this is a process which may take considerable time, and readapting during this transition could be really painful: we may be able to readapt a strategy to something which used to work just a month ago, but then a week or two pass – and it stops working again. Therefore a better solution could possibly be to focus on certain market processes which are less dependent on the general price behavior determined by the market structure.

Since, as we discussed above, processes related to changes in market structure and market regimes are global and always take quite some time, it would be quite natural to suppose that focusing on strategies with somewhat briefer position holding time could potentially improve the performance during the transitional periods and make returns less volatile and prone to changes in the market regime.

Let’s consider a strategy based on the same momentum trade idea, and let’s start to decrease the time in the market (N_Days) from 10 days down to 1 day to see if it helps gaining any new edge in respect to the change in market regimes in question. We will look only at the graphical representation of theoretical returns because such a representation gives a clear idea about how the strategy used to perform during various historical time spans, while integral metrics such as profit factor, Sharpe ratio and other do not present information of this kind.

We can clearly see that reducing the time in the market we observe a substantial increase in the strategy performance before and after the crisis of 2007-2009, but overall the strategy stability is questionable, and it can hardly be traded in real life. The next obvious step would be to look inside a single day to see if we could find any short-term tradable opportunity which would be less sensitive to changes in market regimes.

Let’s consider a medium-term strategy which is based on the same principles as the one we have just discussed, but holds positions only for several hours, so we are talking about an intraday strategy. Let’s look first at its historical performance in regard to its sensitivity to changes in the market structure and consequently market regimes.

Again, like in Fig. 1 above, the vertical blue line denotes the end of the transitional period in the market structure and consequent changes in the market regime caused by Dodd-Frank. We can see that the strategy continues to perform in more or less the same manner as it used to do before this historical period.

At the same time we also can see that this strategy is not ideal and it seriously underperforms between 2004 and 2008. The explanation of this underperformance should be found in another transitional historical period, which, however, is explained by changes in the market structure specific for the fx markets, without significant global impact. It is not surprising because an intraday strategy is always very sensitive to timing, and timing strictly depends on the key events for a given market, such as opening hours, settlement time and so on. Changes in the market regime in fx between 2004 and 2008 were mostly caused by changes in the market infrastructure, we even may say that during that time this market ceased to be a purely interbank market and became more universal. Thus a trading strategies developer should take into consideration not only global changes in market structure and market regimes, but also pay serious attention to market-specific infrastructural developments.

To summarize, we can conclude the following.

- Changes in market structure are the very reasons which may completely destroy any trading strategy which might perform very well before such a change. Therefore besides regular stress-testing we should always perform a robustness test which shows how this given strategy might behave in a changed market environment.

- Reducing time in a position may help increasing the robustness, but at the same time it may make the strategy more sensitive to other changes in the market environment, which sometimes can hardly be distinguished. Besides that reducing the time in the market below a certain threshold may make the strategy not tradable in reality, see our previous article on this subject.

- Ideally we should use a number of different strategies in a portfolio, each of them could be sensitive to changes in the market structure of a certain type, but together they potentially could compensate each other’s underperformance, thus reducing volatility of returns and making gains more consistent.

- In any case, regardless of the type of strategy and the complexity and sophistication of the portfolio in question, live trading should be routinely supervised by the researcher to maintain the consistency of performance and the very trading ideas which lie in the foundation of the trading strategies to the present state of the market structure, and sometimes even stop certain strategies in order to avoid significant losses with uncertain chances of recovery.

— Alex Krishtop